Sending money back to your family with Bitcoin remittances

The existing remittance alternatives, and the back-of-the-envelope math to justify a hypothetical fully managed bitcoin remittance business.

Background

A remittance: http://www.wikipedia.org/Remittance' is defined as a transfer of money from a foreign worker to someone in their home country. In the USA for example, a foreign worker typically sends home around $200 per month (the most common destinations are to Mexico, China, and India). Although this amount may seem small, in aggregate, remittances are extremely significant. In many countries remittance payments are higher than any government foreign aid received, and can make up a significant portion of GDP. Some of the largest remittance pathways in the world include US to Mexico ($21.6 billion per year), UAE to India ($15 billion per year), and Hong Kong to China ($17 billion per year). A beautiful visualization of this data can be found on Pew Reseach Center: http://www.pewsocialtrends.org/2014/02/20/remittance-map/ .'

Current remittance flow pathways

Currently, in order to send money abroad, you would use either informal or formal pathways.

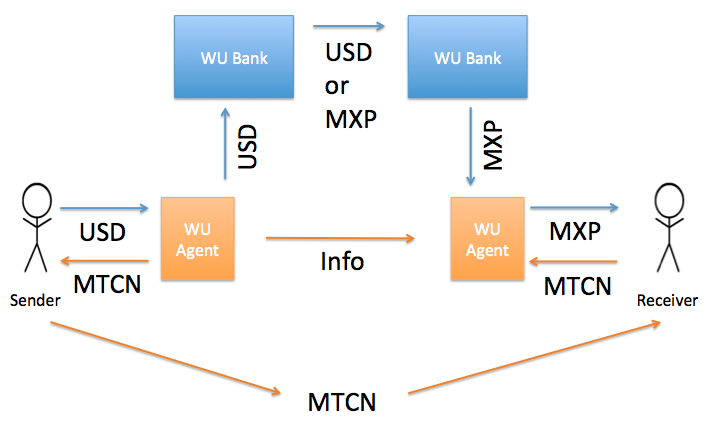

Formal pathways - Western Union/Money Gram/Xoom

The diagram below shows how you might send money via Western Union, Money Gram, or Xoom. First, you would first send money to a Western Union agent (WU Agent). In return they would give you a MTCN (Money Transfer Control Number) to track your request. You would send this tracking MTCN number to the receiver (bottom orange pathway in the diagram). Next, behind the scenes, the WU agent in your home country would inform the WU Agent in the foreign country that this is a valid transaction. Your relative would then be able to visit the agent and receive the money by supplying the MTCN number and identification.

Behind the scenes, the actual money is transferred in a series of transactions between banks and financial institutions, adding overhead and cost to the transaction.

This existing system of relationships adds complexity and thereby cost to the remittance flow. A typical cost of transaction in this system is anywhere from 8-11%. A transaction in this system also relies on trust. The sender and receiver must trust Western Union/Moneygram and the local brokers to act with reliability and integrity. There is the possibility of network outtages and dishonest brokers along the way, which could end poorly for the remitter. Ultimately, a system that relies on trusting a single instution creates a single point of failure, opening the door to frozen accounts, reversals, and red-lining (financial discrimination).

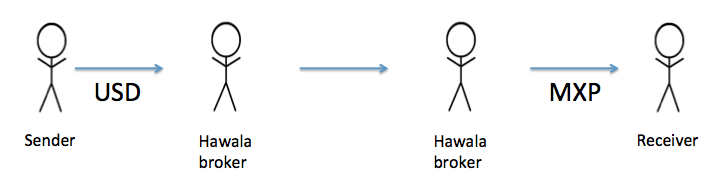

Informal Pathways - Hawala

Hawala is a informal system of money transfer that is very popular in the Indian subcontinent. This system works through a series of informal relationships of brokers based on trust. To send a remittance, you would contact a local Hawala broker. This broker would transmit this information to the foreign Hawala broker. Although this method is often much lower cost than more formal pathways, it is untraceable and completely dependent on trust between brokers. Although Hawala is known for extremely high rates of successful transfer, a system that relies on trust has the same issues discussed above, transfer reversals, untrustworthy brokers, and delays. A typical cost of transaction in this system is anywhere from 1-5%.

Introducing Bitcoin - a whole new pathway!

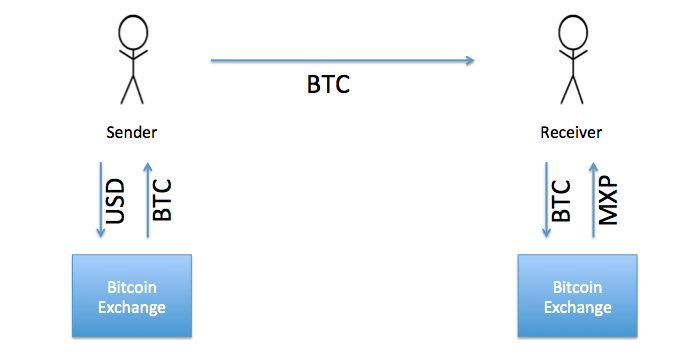

To transmit using purely bitcoin with no intermediary

Using Bitcoin (BTC), a sender could send Bitcoin directly to a receiver. To get Bitcoin to send, they would need to use an exchange that operates in their local currency. Similarily, the receiver would need to use an exhange to get their native currency. This is the best method to use, do to the low transaction cost, but the downside is it requires both parties to be technically savvy enough to understand and use Bitcoin. Neither party needs to trust intermediaries (money brokers, Hawala, etc.), they only need to trust the mathematical certainty of a Bitcion transaction. The cost of this transaction would be the combined cost of the bid/ask spread in each exchange. For USD to MXN this would be <.2%

Split managed Bitcoin remittance system

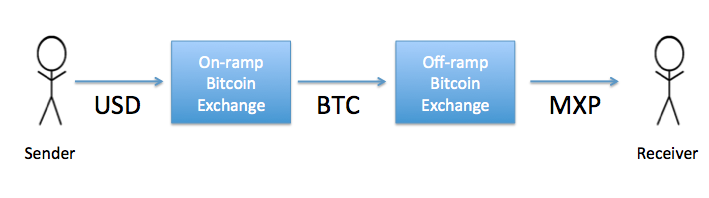

Unfortunately, it is unlikely the person-to-person Bitcoin transfer system will take off immediately because it requires technical ability that the majority of the world does not have. To this end, Bitcoin remittance services have sprung up that promise to transfer from one currency to another, but where neither the sender nor the receiver need to know that Bitcoin is being used behind the scenes. Ideally, sending money to a relative should be a simple as swiping a credit card and going to an ATM.

One way these Bitcoin backed money transfer services are accomplishing this mission is using a split system, where an "on-ramp" and "off-ramp" are separate businesses. In this division, the "on-ramp" business solves the problem of accepting USD and sending Bitcoin. The "off-ramp" service solves this problem by then exchanging those funds for the recipient's currency. Luis Buenaventura of Rebit.ph (an off-ramp service) does an amazing job of explaining how this system would work http://techcrunch.com/2015/01/30/the-bootstrappers-guide-to-bitcoin-remittances.

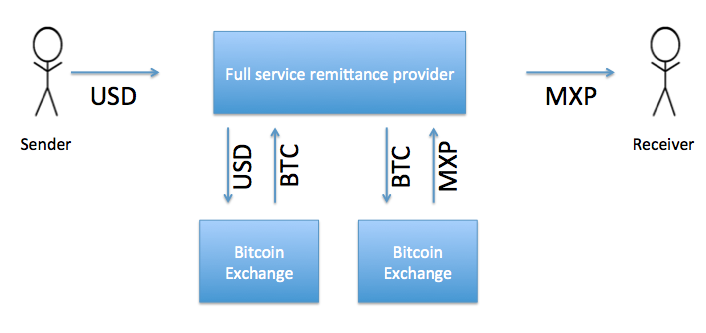

A solution to all problems - fully managed Bitcoin remittance system

A fully managed Bitcoin remittance system would include both the on-ramp and off-ramp systems into one business, allowing a more seamless user experience for the sender and receiver of the payment. For customers used to dealing with Western Union or Moneygram, switching over to just one company, rather than multiple would lower switching costs.

In this sort of system, to an end user, the experience would be as simple as : Going to the site, entering your relatives mobile phone number, your credit card number (or direct deposit to save 3%), and money and frequency of sending, and then the site takes care of the rest. Behind the scenes, the full service remittance provider would be doing the exchange of BTC back and forth to receiving and sending currencies.

Financial Impact

If 1 company decides to pursue to bring all steps of the process in house, and provide first mile all the way to last mile services (the highest potential profits), then due to the nature of remittance flows (rich countries to poor countries), there will be a net currency imbalance. This currency imbalance will be tilted so that there is a surplus of sender currency, and deficit of receiver currency.

To give an example of this, consider the following: As of 2013, the USA to Mexico remittance market was $21.6 billion. Let's break down an example of potential profits as a full service remittance provider (first to last mile). If as a service provider you were to capture 1% of the USA to Mexico remittance market, by providing money transfer services between US dollars (USD) and Mexican pesos (MXN), over the course of the year of doing business, you would end up with $216 million dollars in surplus USD cash (1% of $21.6 billion), and 3.3 billion MXN deficit because of cash dispensed.

The need to balance your books

In order to actually have sufficient MXN in your dispensing account, you would need to be a participant in the forex market to transfer those USD received into Pesos (from an accounting perspective, going from your USD accounts receivable to your Mexican accounts payable).

A bitcoin remittance company would want to avoid exposure to movements in underlying currency, so they would aim to settle transactions immediately. This could take the form of a daily settlement forex trade, where the Bitcoin remittance companies looks at the sum total of transactions for the day (+ X USD, -Y MXN), and then makes the opposite transaction to balance their books (-X USD, +Y MXN).

As of May 7, in the foreign exchange market, with worldwide daily volumes in the trillions of dollars, the Bid/Ask spread of USD to MXN is:

| USDMXN | |

| Bid: | 15.3049 |

| Ask: | 15.3066 |

Calculating cost using (Bid - Ask)/(2 * Market) gives a cost of transaction 1 basis point. (.01% : a basis point is a hundredth of a percent). This assumes no additional trading fees from the forex bank placing your trade, and that they are making their money based on this Bid/Ask spread.

Your spread is transaction cost (assuming only bid/ask spread and no other fees) .01-.00011 = .00989 = 99 bips is profit margin. If you charged half of Western Union rates (which are close to 8%) to stay competitive, you could make .04-.00011 = .03989 profit (3.989% on a transaction). If you captured 1% of the market in our earlier example, you would make $10.4 million in yearly profit.

Of course this doesn't include the costs of developing and maintaining this software solution, as well as marketing, support, charge contesting, etc.; but the market is still very lucrative.

A full scale Bitcoin remittance operator has huge potential to change the remittance market by globally reducing fees and increasing ease of transferring money. As Bitcoin grows, and lowers the cost of worldwide remittances, it will also increase the total remittance market, adding new value and enabling new people to send money. Existing operators (I'm looking at you Western Union), need to quickly adapt to new ways of doing business, or be ruled obsolete by Bitcoin.